The Evolution of Retail

"Next-gen", millennial-focused, direct-to-consumer brands are getting a bad rap. Casper's IPO has flopped, Brandless shut down, and many are cutting staff - what's going on here?

I’ve been thinking a lot about what makes a good company in the digital retail/e-commerce space - it seems like a couple of years ago everyone was railing on brick-and-mortar in favor of e-commerce, and now e-commerce is feeling some pain. In order to understand, I tried to take a look at the timeline of retail to see if there were any interesting trends.

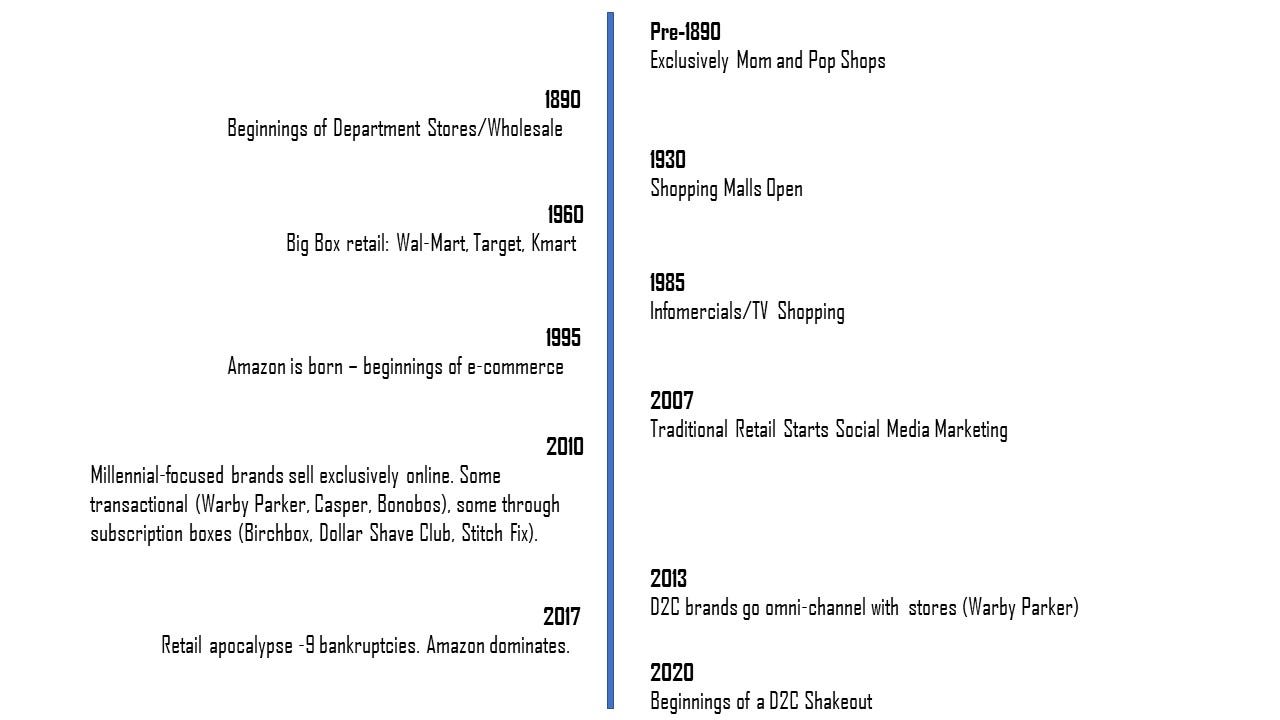

Retail has evolved over time, from mom and pops, to department stores, to full-fledged malls, to e-commerce, and to the eventual weakening of traditional brands. In 2017, most industry analysts were saying brick-and-mortar was dead and Amazon was the murderer. Amazon wins because it makes buying so easy it doesn’t feel like buying - it’s continuous product exploration. I can buy something today, get it in 2 days, drop it off at UPS with only a QR code (no packaging) if I don’t like it, and start the cycle again. However, Amazon has never prioritized having the most premium brands on its platform. We buy on Amazon not because we think the brands are somehow more compelling, but because it’s easier, cheaper and faster than other sites. Amazon left the brand voice exercise to the next-generation of brands, or what we now call direct-to-consumer (D2C).

When these companies first came onto the scene (Warby Parker, Bonobos, Casper, Glossier), their superpower and real innovation was their direct connection to customers; because they knew exactly who their customers were by virtue of selling directly on their websites, they were able to more effectively find out what features people wanted and how to make the product better. Some of these companies were even able to engage their customers from the very beginning by building a fanbase and raising money on Kickstarter (Allbirds, Brooklinen).

*Allbirds Kickstarter Campaign*

However, D2C brands also pitched the ability to sell at higher margins by bypassing the large retailers (who take a cut of revenue). The problem with this argument very quickly became evident - having a website on the internet did not mean these companies could achieve mass distribution. The independent brands were now on the hook to market their products, whereas larger retailers could have helped with distribution and brand recognition. Digital marketing became crucial, and social media platforms were the main beneficiaries of advertising spend. While at first ads on large social media platforms were cost-efficient, the more brands and users entered the market -> the higher the demand for brand advertising -> basic economics meant the platforms could raise prices.

With heavy dependence on Facebook/Instagram and rising costs, the e-commerce brands began to look back to brick-and-mortar for its reach and branding capabilities. Bonobos opened its first store in 2012, and Warby Parker in 2013.

Casper opened its first store much later, in 2018 (and perhaps it was too late, given the nature of the product and the company’s current outsized investment in digital marketing). Today, companies like Leap exist in order to create turnkey stores for D2C brands. These brands have gone omni-channel.

Obviously digital and physical marketing will still be necessary; the best brands throughout history grew via great advertising, but smart companies will be more efficient about how they target. Gone will be the hordes of niche ads on NYC subways, like Figs, which sells scrubs and medical apparel. These ads get wide reach, but there are probably way more efficient and targeted places to market scrubs (though to caveat, I have no visibility into their financials and ROI on this campaign, so I’m really just conjecturing here).

I’ve generally found that wider reach isn’t always more effective. I post unpaid surveys from time to time in Facebook groups to do research, and I find that smaller groups with 500-1k members drive more responses than groups with 5k+. In addition, I hear more and more e-commerce companies saying that they see higher sales conversions when partnering with micro-influencers vs. Instagram models with huge follower counts, mainly due to higher engagement.

Having walked through this analysis, I would say my key learnings are:

Cost-reduction was not necessarily the place where D2C brands could innovate.

Companies would have to diversify and be more targeted with marketing spend.

The direct customer connection and ability to build better products remained the key differentiator. I now believe the best D2C companies will be ones that leverage this superpower to create best-of-breed products, ones that speak for themselves and attract eyeballs without outsized sums of marketing dollars.

With all of this in mind, I believe 2020 will be a year of reflection and re-calibration for this market. These companies will be forced to trim down, prioritize profitability, and be smarter with their venture capital money - and it starts with coming back to what made these companies great to begin with: a deep customer connection.